5 ways to protect your money in the cost of living crisis

Posted by JSCFinancial on Tuesday 14th of March 2023.

With inflation at its highest level in 41 years and energy prices skyrocketing, the cost of living crisis has dominated headlines since inflation began to creep up from historic lows in mid-2021.

While the Covid pandemic began the inflationary increase, this was further exacerbated by the war in Ukraine pushing up energy and food prices even further.

Following such an extended period of price rises, you may be concerned about your household finances and long-term plans. So, here are five ways to protect your finances during the cost of living crisis.

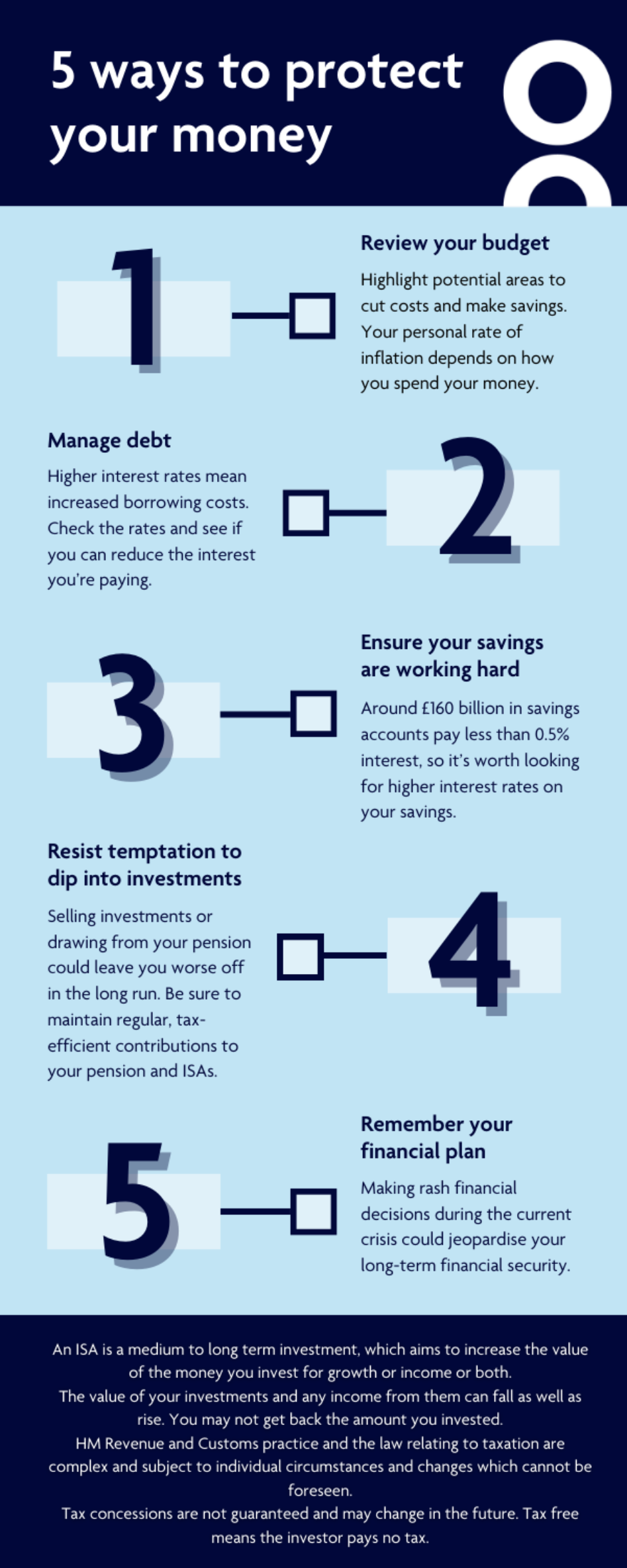

Review your budget and personal inflation rate

Reviewing your spending will clarify where your money is going and highlight potential areas to cut costs and make savings.

Despite a lot of noise about inflation and its impact on UK households, the good news is that your personal rate of inflation depends on how you spend your money. It won’t necessarily match the official inflation rate and so changing your spending habits can help bring it down.

For example, since much of the rise in prices has been caused by soaring fuel prices, your personal inflation rate may be lower than the average if you don’t drive or own a car.

Energy prices have also risen significantly throughout 2022. However, if your home is especially energy-efficient, you may use less energy than an average household. This could bring your personal inflation rate below the average.

You can use an online calculator – such as this one from the ONS website – to help you work out your personal inflation rate online.

Manage debt

Higher interest rates mean increased borrowing costs. So, check the rates and see if you can reduce the interest you’re paying.

Focus on repaying credit card debt first. Credit cards typically charge high levels of interest and the negative compounding effects can be difficult to escape.

If you have high credit card debt, transferring to a limited-period nil-interest rate account could help you repay the debt sooner.

Ensure your savings are working hard for you

Around £160 billion in savings accounts pay less than 0.5% interest, so it’s worth shopping around for higher interest rates on your savings.

Alternatively, Insignis can help you secure the best cash savings rates.

As interest rates change, Insignis moves your money to secure optimal rates. The one-time sign-up is quick and easy to set up, plus you’ll never need to open or close another account again.

Resist the temptation to dip into your investments or stop saving for your future

You may be tempted to dip into your pension or investments to tide you over but consider the long-term effect on your retirement plans.

Selling investments or drawing from your pension could leave you worse off in the long run, so assess every option before you act.

It’s important to continue to pay your future self first, too; be sure to maintain regular, tax-efficient contributions to your pension and ISAs.

Remember your long-term financial plan

Making rash financial decisions during the current crisis could jeopardise your long-term financial security. If you’re worried about the rising costs of living and what you can do to protect your short- and long-term financial plans, we can help.

Get in touch

If you’re worried about the rising cost of living and would like to discuss ways to protect your finances from the effects of inflation, we’re here to help. Please get in touch to arrange a time to chat.

An ISA is a medium to long term investment, which aims to increase the value of the money you invest for growth or income or both.

The value of your investments and any income from them can fall as well as rise. You may not get back the amount you invested.

HM Revenue and Customs practice and the law relating to taxation are complex and subject to individual circumstances and changes which cannot be foreseen.

Tax concessions are not guaranteed and may change in the future. Tax free means the investor pays no tax.

Approved by The Openwork Partnership on 14.02.2023

Please note: by clicking this link you will be moving to a new website. We give no endorsement and accept no responsibility for the accuracy or content of any sites linked to from this site.