Saving for a university education

Posted by JSCFinancial on Monday 13th of June 2022.

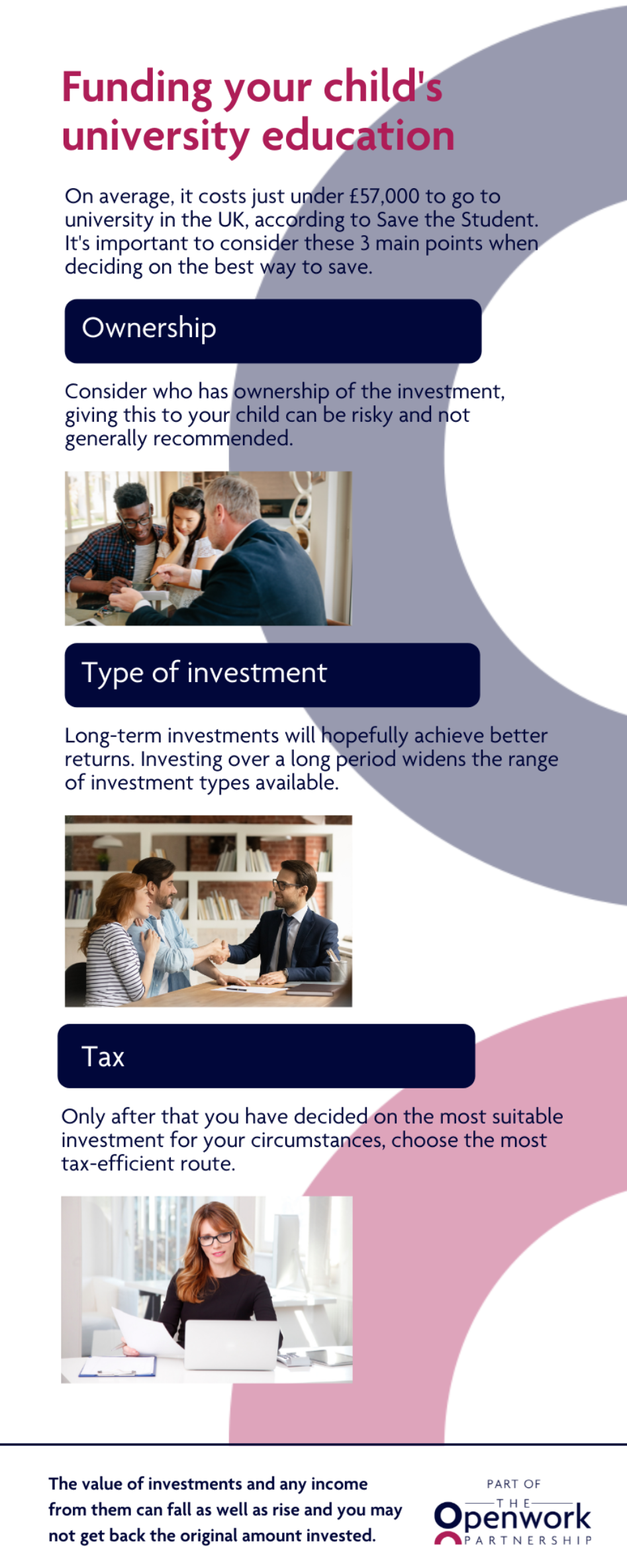

Funding your child's university education

Sarah and Andrew’s 10-year-old twins, Isabelle and Isaac, couldn’t be more different. While Isabelle is boisterous and full of beans, Isaac is gentle and reserved. The children do have one thing in common though - they’re both extremely bright and they already know exactly what they want to do when they grow up. Isabelle loves animals and wants to be a vet; and Isaac is a very talented artist and has his heart set on art school.

When they found out they were getting two for one, Sarah and Andrew couldn’t have been happier. But bringing up twins hasn’t been cheap and the couple are aware that as the children grow so will the strain on their finances. Having heard stories about the ever-rising cost of higher education, Sarah and Andrew are particularly keen to start saving for the twin’s university education.

How much does university cost?

On average, it costs just under £57,000 to go to university in the UK, according to Save the Student. This figure is based on the fact that the cost of tuition for most students is about £9,250 a year, average living costs are £9,720 a year and the majority of undergraduate degrees last three years. However, the exact cost can vary quite a lot depending on where you study and the course you’re doing. If Isabelle still wants to become a vet after doing her A-levels, she’ll be looking at going to university for five or six years so her costs will be higher than average. As well as a tuition fee loan, students can get a maintenance loan to help cover living costs. However, the average maintenance loan is only about £5,640 a year so there is more than likely going to be a significant shortfall.

Where should Sarah and Andrew start?

The good news for Sarah and Andrew is that they’ve started thinking about saving early. With at least eight years before the twins go to university, if their parents start saving straight away there is plenty of scope for their investments to grow.

The first thing Sarah and Andrew should do is get advice from an expert. This will help to ensure they make the right investment decision for their particular circumstances and avoid potential pitfalls.

What will Sarah and Andrew need to consider?

There are three main points Sarah and Andrew will need to consider when deciding on the best way to save for Isabelle and Isaac’s future:

- Ownership

Sarah and Andrew will need to decide whether to give ownership of the investments they make to Isabelle and Isaac. This is not generally recommended as it would mean the twins could cash that investment and blow the lot on their 18th birthday (16th if they were living in Scotland).

- Type of investment

As Isabelle and Isaac are still quite young, Sarah and Andrew have the option of making long-term investments that will hopefully achieve better returns. Being able to invest over a long period will widen the range of investment types available to Sarah and Andrew. Once they’ve made their initial investments, they would be well advised to review them on a regular basis to make sure their money continues to work as hard as possible.

- Tax

Sarah and Andrew shouldn’t choose their investment based on tax. However, once they’ve decided on the most suitable investment for their circumstances, it makes sense to invest via the most tax-efficient route.

If you’d like to discuss investment options for your child’s university education, we’ll be happy to help.

The value of investments and any income from them can fall as well as rise and you may not get back the original amount invested.

Key takeaways:

- The earlier you start saving, the better. This opens up the possibility of long-term investments offering potentially higher returns.

- Get advice from a professional to help ensure you make the right investment choice first time.

- Consider who’ll have ownership of the investments – giving ownership to a child can be risky.

- Review long-term investments on a regular basis.

- Once you’ve chosen your investment, make sure you invest via the most tax-efficient route.

Please note: by clicking this link you will be moving to a new website. We give no endorsement and accept no responsibility for the accuracy or content of any sites linked to from this site.